How are government monopoly cannabis retail sales working in Canada? Pretty well, maybe. There’s a lot to learn.

Most provinces allow private retailing. Two of those that don’t, Quebec and Prince Edward Island, have reportedly done the best at capturing market share from bootleggers.

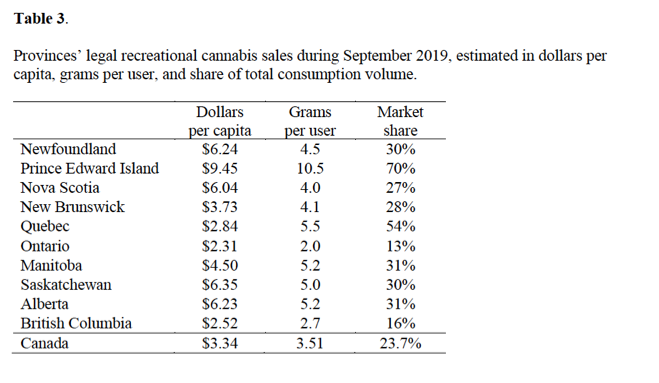

Brock University Business School Professor Michael J. Armstrong presents this data:

Michael J. Armstrong, “Legal cannabis market shares during Canada’s first year of recreational legalisation”, International Journal of Drug Policy, Volume 88, February 2021, 103028,

https://doi.org/10.1016/j.drugpo.2020.103028.

I don’t know how much to make of that data, which is now old. Ontario was having trouble then, and at one point switched from government to private retailing. But government monopoly retailing in two provinces was reportedly doing well at defeating the illegal market.

Beyond market share, “[i]n 2019, Quebec’s monopoly marijuana retailer – Société québécoise du cannabis (SQDC) – said it would not carry cannabis vaporizers ‘in the light of many health problems.’ Quebec also bans ‘sweet or savory edible products,’ including marijuana-infused chocolates, as well as all topical cannabis products.” https://mjbizdaily.com/legal-cannabis-sales-in-gatineau-quebec-collapse-after-age-requirement-hike/

Maybe that’s a bug, driving consumers to bootleggers, or to neighboring provinces. Or maybe it’s a feature, keeping consumers away from vaping (when was that vaping scare, anyway?) and keeping kids away from cannabis candy.

Lots to think about.