I don’t think “a $1 increase in cannabis taxes leads to a $3.91–$6.32 increase in cannabis prices.”

Email sent 30 June 2026

Dear Dr. Park:

Congratulations to you and your colleagues (whose email addresses I do not have) on your thought-provoking and detailed article, “The impact of taxes on prices and the demand for legally sold recreational Cannabis in the U.S.” I appreciate your work in this evolving field.

Please let me know if this message reaches you.

I write as a tax policy lawyer who has worked on cannabis tax policy since 2011. I’m a member of the North Carolina Advisory Council on Cannabis, and a Council colleague sent me your article. To reveal my bias, your article states what I’ve long thought: that cannabis taxation can help in “[p]reventing and reducing adverse cannabis use such as cannabis use disorders, and generating tax revenue.” But, as you point out, “while increasing cannabis excise taxes reduces legal demand significantly, it is likely that consumers may purchase illegal products instead.”

So my advocacy for marijuana taxation was taken aback when I read the conclusion, “a $1 increase in cannabis taxes leads to a $3.91–$6.32 increase in cannabis prices.” Such a price increase could send many consumers to illegal products.

So I have wondered about that conclusion. There’s a lot I don’t understand that you do understand, and I hope to approach this matter with humility and curiosity.

I

Most U.S. state taxes are simple add-on ad valorem at retail – where a $1 increase in taxes will increase prices less than $1, if the seller bears some of the burden.

How much less? Hansen et al say “we find that consumers bear about 44 percent of the retail tax burden.” https://www.nber.org/system/files/working_papers/w23632/revisions/w23632.rev0.pdf

I understand that in imperfectly competitive markets, overshifting above 100% is theoretically possible — firms can use a tax increase as cover to raise prices further than the tax requires, particularly in concentrated markets. Your paper cites this dynamic, drawing an analogy to cigarettes and alcohol, and several studies (Hollenbeck & Uetake, 2021; Mace et al., 2020) describing cannabis markets as local monopolies. I don’t dismiss that mechanism. But I’m told that even the empirical overshifting literature on cigarettes and alcohol — the closest analogues you cite — generally finds pass-through in the range of 100-150%, not 300-600%. Are there comparable magnitudes elsewhere in the literature, — or what is structurally different about cannabis markets that would produce overshifting an order of magnitude larger than these analogues?

II

A handful of states, like Canada, tax upstream of retail. But only a few.

Now I can make up a case where a $1 tax far upstream adds an extra $3 to the consumer’s price, but I know of no real cases even approximating the facts in that made-up case. Compound levels beyond three and you can get to $4, but only in Theoryland.

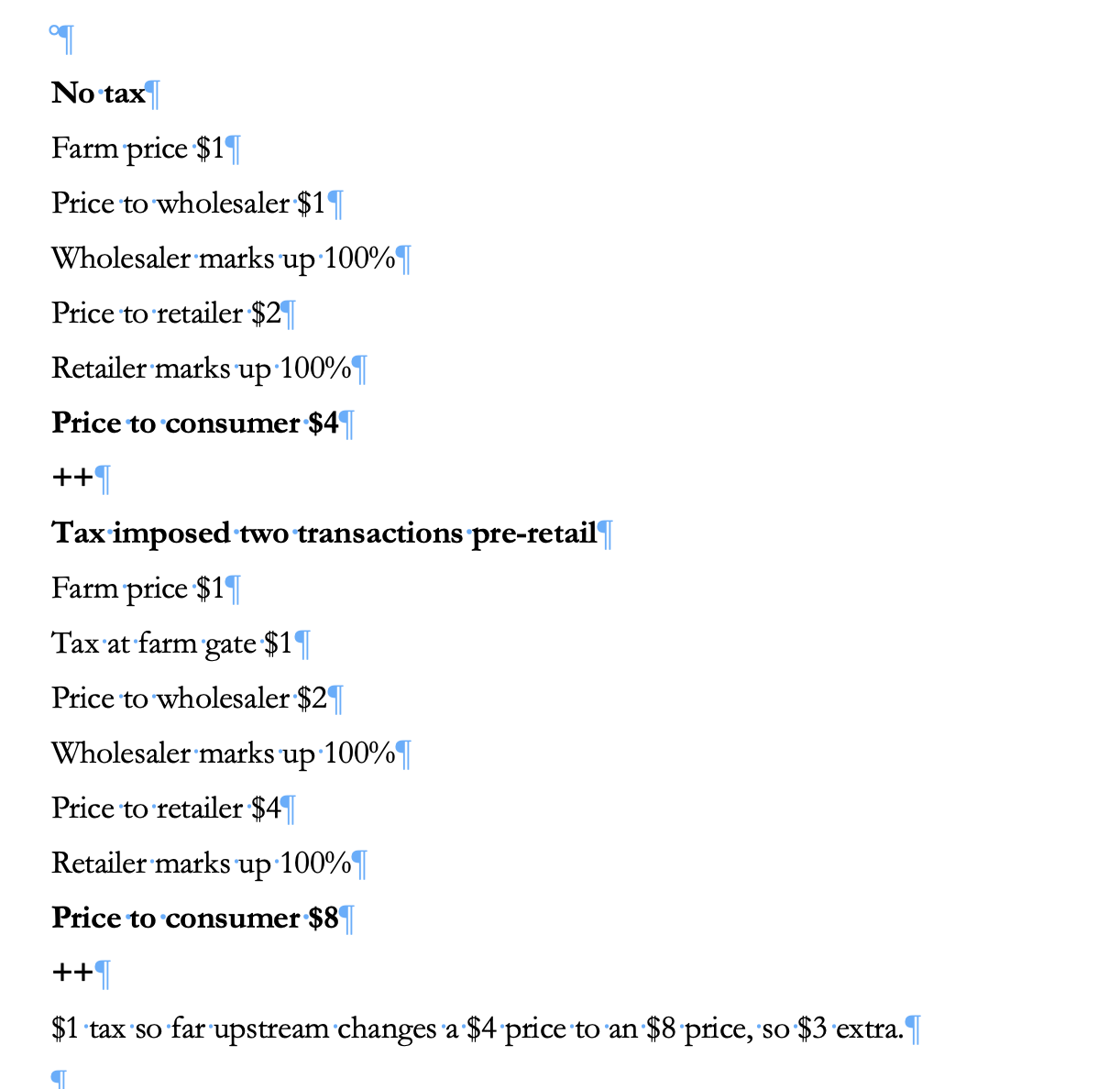

This is an extreme example.

No tax

Farm price $1

Price to wholesaler $1

Wholesaler marks up 100%

Price to retailer $2

Retailer marks up 100%

Price to consumer $4

++

Tax imposed far upstream pre-retail

Farm price $1

Tax at farm gate $1

Price to wholesaler $2

Wholesaler marks up 100%

Price to retailer $4

Retailer marks up 100%

Price to consumer $8

++

Given that only a handful of states tax upstream of retail, and even this deliberately extreme hypothetical only reaches $3 in additional pass-through, I have difficulty seeing how the $3.91-$6.32 range could be reached through upstream tax structure alone — which leaves overshifting or methodology as the more likely explanations.

A colleague pointed out that my hypothetical implicitly assumes the farmer’s pre-tax margin is preserved untouched, with the wholesaler and retailer absorbing nothing and the consumer absorbing everything via two successive 100% markups. In practice, I am told, the empirical tax-incidence literature suggests upstream sellers often absorb at least part of a new tax rather than passing it through at full markup multiples — which would make my $3 estimate an upper bound, not a typical outcome. If the farmer bears some burden, as, I am told, standard incidence theory and the Hansen et al. findings in Part I suggest, the real-world pass-through would fall well short of even my “extreme” hypothetical.

III

Justin Leiby, Professor of Accounting at the University of Illinois, alerted met to this issue and explained it as a circularity. As I understand it, your methods section states that for ad valorem tax states, the standardized cannabis tax variable was constructed as the statutory rate multiplied by the time-varying state-level cannabis price. In Table 4’s pass-through regression (Equation 4), this same price-derived tax variable is then apparently regressed against cannabis price as the dependent variable. For these states, doesn’t this construction guarantee a positive mechanical relationship between the regressor and the dependent variable, independent of any real economic pass-through? I wonder what share of your sample’s tax variation comes from ad valorem states (the vast majority) versus weight-based or potency-based states, and whether the $3.91-$6.32 pass-through estimates are robust to restricting the sample to the handful of non-ad-valorem states only, where this circularity would not apply? Or am I missing something?

To restate that point no doubt repetitiously, Professor Leiby raises what sounds like a fundamental methodological concern: if the tax variable in ad valorem states is constructed as (statutory rate × retail price), and retail price is also the dependent variable, the regression may be finding a mechanical relationship rather than a causal one. A regression of P on 0.15P will produce a large coefficient on the tax variable almost regardless of any real-world relationship between taxes and prices. If that’s what’s happening, the $3.91-$6.32 figure may be a statistical artifact. Can you help me understand how the model addresses this?

I hope this response is useful, but as a lawyer, I may be way off.

++++

Other issues

This statement seems overbroad: “increasing cannabis excise taxes leads to a significant decrease in tax revenue collection.” Not always. It depends. The tax “Laffer curve” may come into play. https://www.investopedia.com/terms/l/laffercurve.asp. Hollenbeck and Uetake wrote, “Washington’s 37% excise tax is still on the upward sloping portion of the Laffer curve and state revenue could be substantially higher with a higher tax rate.” https://www.anderson.ucla.edu/documents/sites/faculty/review%20publications/research/wa_taxation.pdf

I might question the following conclusion, too, as unexplainable as to causation: “a 10% increase in higher cigarette taxes significantly reduce [sic] legal recreational cannabis sales by 9.1%.” But I don’t care about that issue.

Typos:

I always appreciate people pointing out typos as my work progresses, so here are a few:

While studies on taxation is lacking.

Estimates of the priced elasticity for cannabis demand is outdated

we assess that the cannabis taxes is not a weak instrument (

The average taxes based on varying prices in 2022 dollars was

a 10% increase in higher cigarette taxes significantly reduce legal recreational cannabis sales by 9.1%.

Other substance taxes (: $ per pack including federal taxes . . . ; Colon placement: Other substance taxes: ($ per pack including federal taxes . . .

++++

What a great and challenging new field to work in! Thank you for what you are doing. I hope we can circulate this discussion to interested persons. I have a lot to learn and look forward to hearing from you.

With respect and appreciation and goodwill,

Continue reading “An issue with an article about cannabis taxes”