Pending Congressional restriction of Farm Bill Hemp THC Drugs will tax them. Proposals before Congress would classify these drugs as “marijuana,” and put them into Schedule I of the Controlled Substances Act, at least for now. All Schedule I substances are subject to the 280E selling expense tax.

Will the Joint Committee on Taxation score this revenue gain?

Must this kind of back door revenue raising bill originate in the House?

Does this legislation violate Grover Norquist’s No Tax Pledge — and set up primaries for the bill’s supporters? Grover famously tolerates “marijuana” taxes, since they involve a liberating move from prohibition to taxed sales. But cracking down on Farm Bill Drugs means moving from a free market to regulation and from untaxed sales to taxed sales. Is there some exception to the No Tax Pledge for “loophole closers”? Lots of tax increases that need to happen are loophole closers.

Now I suspect that the 2018 Farm Bill “loophole” that carved hemp drugs out of taxed “marijuana” was not scored as a revenue loser. But supposedly no one knew that that bill was legalizing intoxicants.

“With hemp THC drugs wide open 24/7 and unregulated in North Carolina now, I see no chance that they will be fully prohibited. So I think the only hope for North Carolina is to regulate them.” — I wrote that in September, but now in November that Congress is treating hemp like marijuana, I’m not so sure. Here’s what I thought back then:

There’s speculation that the Trump Administration might reschedule cannabis into Schedule II rather than the predicted Schedule III. That sounds doubtful. To exhaust the possibilities, here’s another doubtful option — a little light-hearted speculation.

President Trump has said the following about cannabis—

“I’ve heard great things having to do with medical, and I’ve had bad things having to do with just about everything else. But medical, and, you know, for pain and various things.”

What if he wanted rescheduling for only medical cannabis into Schedule III, while leaving adult-use in Schedule I? It sounds crazy, but anything can happen these days, and President Trump calls the shots.

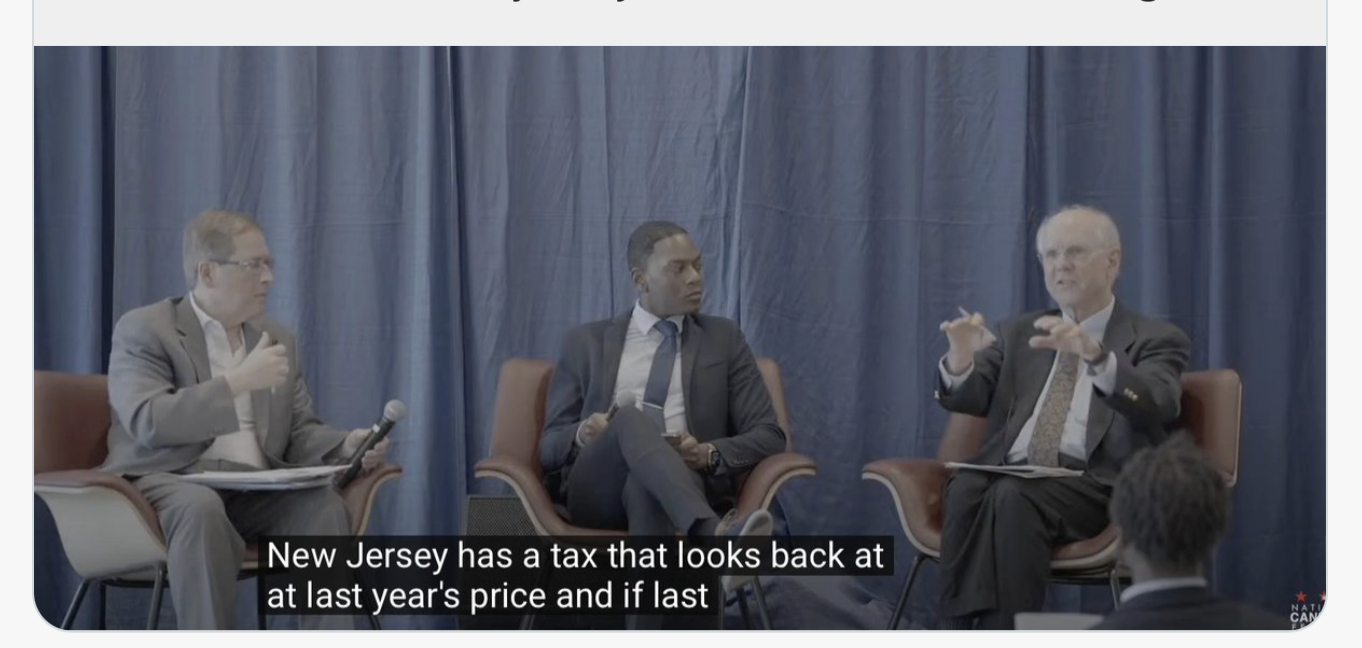

I’m as big a fan of a potency tax as you can find, so I’m sad to say that New York repealed its THC tax in 2024. https://mjbizdaily.com/most-new-york-marijuana-operators-save-big-without-potency-tax/ Legal sellers in New York were having so much trouble competing with illicit sellers that they succeeded not only in reducing the tax burden but in changing the tax base from milligrams of THC to an ad valorem (percentage of price) tax. I think people in state government were desperate to give legal sellers any relief they asked for.

Still, Connecticut continues its THC tax, as does Canada. Bravo. Illinois’s weird little combination tax is still on the books. It taxes products more heavily if they cross the 35% THC line with a higher ad valorem rate. The intent was to tax flower at a lower rate than concentrates, which would have been doable, but they somehow landed on this bright line 35% threshold, which is not ideal technically.

After this post, the NC House stripped out the CBD ban and ended up with only age-gating at 21. The bill moves on to the Senate as of June 26, 2025.

Here’s the original post, for the record:

++++++

The primary intoxicant in marijuana or cannabis is THC. CBD, meanwhile. is universally acknowledged to be non-intoxicating .

But the North Carolina Farm Bill Drug bill that passed the Senate and is heading for the House allows THC but bans CBD. That’s crazy!

A Legislator told me I’m missing something — so I may be wrong here. But I offered a reward on Twitter or X for an explanation of what I’m missing, with no takers.

Let’s take a CBD gummy with no THC of any kind. I think it’s a “prohibited hemp-derived consumable product” under North Carolina House Bill 328.

Sure, a state marijuana monopoly would be federally illegal. I used to think it would be bulletproof as a practical matter, in light of Louisiana’s experiment. But President Trump might pick on states that he disfavors, as he does with California localities and ICE. https://www.msn.com/en-us/news/politics/ar-AA1GMkuT

Louisiana’s two land grant state universities had a state monopoly to produce medical marijuana for years before private industry shoved them aside. Here’s a photo from the HBCU, whose inclusion in legislation may have helped with social equity concerns:

In a 2013 North Carolina poll, state marijuana sales beat private sales by 3-to-1. The full poll with cross-tabs is at https://newrevenue.org/wp-content/uploads/2013/03/nc-marijuana-polling-march-2013.pdf. Not only do monopolies work best for public health, avoid all kinds of litigation by disappointed license applicants, maximize public revenue, and allow nimble pricing (unburdened by inflexible taxes) to compete with the illicit market; as our Stanford friend Keith Humphreys says, in light of the poor track record of social equity licensing, “In general retail monopolies (that’s where the industry still produces the product; the state sells it) have a better record of hiring diverse employees than do private companies.”

President Trump might leave state marijuana sales in Red-State New Hampshire alone, but he might pick on North Carolina, with our Democratic Governor. It’s about how much risk a state wants to face.

“Pat Oglesby Appointed to Marijuana Legalization Commission

“The governor of NC, Josh Stein, has come out in favor of marijuana legalization and formed a commission, on which my co-teacher, Pat Oglesby, has been tapped to serve, to study the issue and make recommendations.

“This is an outstanding choice! Pat knows more about marijuana legalization, taxation, licensing, and related issues than anyone I know. We co-taught a course, Cannabis Legalization, at UVA Law that was a huge success, due to Pat’s knowledge and connections to industry experts, regulators, and researchers (and to our excellent students, of course).

“The official press release is here, which includes the full list of commission appointees.”

Governor Stein Announces State Advisory Council to Bring Order to Cannabis MarketKids Need Protection

RALEIGH, NC

(RALEIGH) Today Governor Josh Stein released the following statement on the need to protect young people by bringing order to the unregulated cannabis market:

“Today all across North Carolina, there are unregulated intoxicating THC products available for purchase: just walk into any vape shop. There is no legal minimum age to purchase these products! That means that kids are buying them. Without any enforceable labeling requirements, adults are using them recreationally without knowing what is in them or how much THC there is. Our state’s unregulated cannabis market is the wild west and is crying for order. Let’s get this right and create a safe, legal market for adults that protects kids.

“That is why I am announcing a State Advisory Council on Cannabis. I am charging this group with studying and recommending a comprehensive approach to regulate cannabis sales. They will study best practices and learn from other states to develop a system that protects youth, allows adult sales, ensures public safety, promotes public health, supports North Carolina agriculture, expunges past convictions of simple THC possession, and invests the revenues in resources for addiction, mental health, and drugged driving detection.

“I want to thank members of the General Assembly for their interest in addressing this gaping loophole in state law. Let’s work together on a thoughtful, comprehensive solution that allows sales to adults and that is grounded in public safety and health. We can work together and get this right.”

Governor Stein signed the Executive Order creating the Council on Tuesday morning. The Council will include representatives from the Office of State Budget and Management, the State Highway Patrol, the Eastern Band of Cherokee Indians, the General Assembly, and the Departments of Health and Human Services, Public Safety, Revenue, Transportation, and Justice.

Hemp and marijuana are both types of cannabis. The difference used to be how much THC was in the plant. Today, due to the cannabis industry’s unchecked and creative product development and packaging, the terms “hemp” and “marijuana” have lost their traditional meanings and are essentially the same thing. They both contain intoxicating levels of THC. As a result, anyone, no matter their age, can legally buy cannabis products in vape shops with high concentrations of intoxicating THC here in North Carolina. The status quo of zero protection of our kids is absolutely unacceptable. That’s why the work of this Advisory Council to recommend a regulatory structure for cannabis sales is important and urgent.

In the meantime, at a minimum, the General Assembly should prohibit the sales of products that contain intoxicating THC to anyone under 21 by requiring photo ID age-verification and require packaging that lets adults know what is actually in cannabis products, including the amount of THC.

Co-chairs

Lawrence H. Greenblatt, MD, State Health Director & Chief Medical Officer, North Carolina Department of Health and Human Services

Matt Scott, District Attorney, Prosecutorial District 20 (Robeson County)

Members

David W. Alexander, Owner and President, Home Run Markets, LLC

Arthur E. Apolinario, MD, MPH, FAAFP, 2002-2023 Past President, North Carolina Medical Society; Family Physician, Clinton Medical Clinic

Joshua C. Batten, Assistant Director for Special Services, Alcohol Law Enforcement Division, North Carolina Department of Public Safety

Representative John R. Bell, North Carolina House of Representatives, District 10

Carrie L. Brown, MD, MPH, DFAPA, Chief Psychiatrist, North Carolina Department of Health and Human Services

Mark M. Ezzell, Director, North Carolina Governor’s Highway Safety Program, North Carolina Department of Transportation

Anca E. Grozav, Chief Deputy Director, North Carolina Office of State Budget and Management

Representative Zack A. Hawkins, North Carolina House of Representatives, District 31

Colonel Freddy L. Johnson, Jr., Commander, North Carolina State Highway Patrol

Michael Lamb, Police Chief, City of Asheville Police Department

Peter H. Ledford, Deputy Secretary for Policy, North Carolina Department of Environmental Quality

Kimberly McDonald, MD, MPH, Chronic Disease and Injury Section Chief, Division of Public Health, North Carolina Department of Health and Human Services

Patrick Oglesby, Attorney and Founder, Center for New Revenue

Forrest G. Parker, CEO / General Manager, Qualla Enterprises LLC / Great Smoky Cannabis Company

Senator Bill P. Rabon, North Carolina Senate, District 8

Lillie L. Rhodes, Legislative Counsel, Administrative Office of the Courts

Gary H. Sikes, Owner, Bountiful Harvest Farm and Partner, Legacy Fiber Technologies

Senator Kandie D. Smith, North Carolina Senate, District 5

Keith Stone, Sheriff, Nash County

Joy Strickland, Senior Deputy Attorney General, Criminal Bureau of the North Carolina Department of Justice

Deonte’ L. Thomas, Chief, Wake County Public Defender Office

Missy P. Welch, Director of Programming (Permits/Audit/Product Sections), Alcoholic Beverage Control Commission

For history, here are results of local votes on marijuana taxes in California at the time of legalization in 2016– from http://www.drugsense.org/dpfca/votersguide1116.html#LOCALS. Voters liked marijuana taxes better than they liked marijuana legalization. At the end is more detail about counties’ results.

In summary, here’s the percentage of votes for local taxes vs. votes for statewide Proposition 64. These are all the counties where a direct comparison is available.

Calaveras County 67 for local taxation vs 47 for Prop 64

Adelanto – Measure R would impose an excise tax of up to 5% on all types of commercial marijuana activities. PASSED 67-33%

Avalon – Measure X would permit up to two medical marijuana dispensaries, and permit the delivery, cultivation, manufacture and processing of medical marijuana products, subject to a $10,000 annual license tax and a 12% transaction fee/tax on each individual medical marijuana sale. FAILED 36-64%.

Butte County – Measure L would permit commercial cannabis cultivation, distribution, manufacturing and transporatation in most zones, while prohibiting outdoor cultivation in residential zones and establishing an exemption for personal cultivation of up to 100 square feet, and collective cultivation of up to 500 square feet. Read more.FAILED 42.5-57.5%.

Calaveras County – Measure C would impose a $2/square foot commercial cannabis tax on outdoor/mixed light cultivation until the state establishes a track and trace program, at which point the tax will be $45/pound of dry weight trim and $10 per pound of dry weight trim; and $5/sq ft. on indoor culivation until a track-and-trace program is implemented, at which time the tax will be $70/lb. of bud and $15/lb. of trim; and a 7% on gross proceeds from manufacturing or retail medicinal or legal cannabis. Would require legal water source and compliance with regulations issued by the Water Quality Control Board, Fish and Wildlife, etc. PASSED 67-33%.

What if the best way to tax cannabis is by potency, by applying a tax rate to measured quantities of intoxicants, like of THC? Two hard questions loom. Should the same per-milligram tax rate apply to intoxicants in various forms of cannabis products like raw plant material (like flower) and concentrates and edibles? And what tax rates should apply to cannabinoids other than delta-9 THC, like delta-8 and delta-10?

For the second question (Let’s say the best way to tax cannabis is by potency, by applying a tax rate to measured quantities of intoxicants, like of THC? What tax rates should apply to compounds other than delta-9 THC, like delta-8 and delta-10 and HHC, based on relative intoxicating power?) here’s a quick answer (that I in no way vouch for, because no one knows) from perplexity.ai, based apparently on https://therichardrosereport.com/cannasearch-daily-news/:

To design an effective cannabis potency tax framework that accounts for different intoxicating compounds like delta-8, delta-9, delta-10 THC, and HHC, tax rates should reflect their relative psychoactive strength and metabolic impacts. Here’s a science-based approach informed by current research and existing tax models:

Relative Intoxicating Power & Tax Multipliers

Compound

Potency Relative to Delta-9

Proposed Tax Multiplier*

Delta-9 THC

1x (Baseline)

1.0

HHC

0.7x-0.8x

0.75

Delta-8 THC

0.5x-0.6x

0.55

Delta-10 THC

0.3x-0.4x

0.35

*Multipliers adjust tax rates based on compound strength compared to delta-9

In 2009, I was a 62-year old lawyer looking for a pro bono project. My career in law at its high point was designing tax laws for Congress — writing laws to bring in revenue — as a staffer for the Joint Committee on Taxation and then the U.S. Senate Finance Committee.

I started with marijuana taxation back then for several reasons.

1 . I didn’t think people should get arrested for possession. Taxation is the main reason and sometimes the only reason that some voters and representatives want to move beyond prohibition.

2. I’m a tax and spend Democrat. That last reason makes industry people and even activists nervous, but OK.

3. It was fun to think about. The field was wide open. No tax professionals were studying it — industry didn’t really exist to study it, and tax academics turn up their noses at marijuana taxation because they think both excise taxes and subnational taxes are not important. The top people in drug policy were interested, but they had only a nodding acquaintance with tax policy.

4. I figured that possession would get legal, and that commerce was sure to follow, and so was taxation. Marijuana tax policy would get interesting.

It has lots of discussion about the tax base but very little about the tax burden, except for this kind of thing: “Tax rates on marijuana need to be low at first to gain advantage in the inevitable price war against bootleggers. As taxing authorities win that war, they can raise rates and generate more revenue.”

Oh, and in 2009, Obama had said, “Yes we can,” and I figured marijuana taxation could be my little part.

{kind=link}

{kind=link}