Many of my friends who support marijuana legalization analytically point with satisfaction to taxes that marijuana brings in. Maybe my scheme to beat Colorado’s new marijuana producer tax procedure doesn’t work. I don’t condone or encourage cheating — au contraire. But I would be nervous that Colorado’s tax is beatable around the edges — not to let people pay zero tax, just to pay less than they owe. Continue reading “Is Colorado’s new marijuana tax leaky?”

NV’s marijuana tax model for MA

When I decided to study cannabis revenue, the most advanced thinking I could find early on was that of Dick Evans, a Northampton MA lawyer. My first footnote in my first article , saying his website was then “probably the most comprehensive compilation of information about laws to tax marijuana” in the world, was a tip of the hat to Dick, who got me going in March 2010 by having me testify before a committee of the Massachusetts Legislature (which wasn’t much interested).

Dick has an opinion piece in the Boston Globe, and I agree with some of it – especially the last part. The title is, “On marijuana law, the Legislature is fixing something that isn’t broken.”

But here’s Dick’s conclusion:

“Allow the voter-enacted law to be implemented, tweaking it only to make up for the lost time. Let the bureaucrats do their jobs. Let people know where to file applications.

“Let’s catch up to Nevada.”

+++

So he’s not opposed to tweaking. And I’m with him on Nevada. While I don’t think Dick necessarily had tax improvements and increases in mind, it’s worth noting that the Nevada Legislature took what the voters had done but then improved the tax structure: The Legislature increased the tax on medical at the pre-retail level and added a brand new recreational retail tax. Not only that, they are pioneering a new weight tax, with new categories that Colorado doesn’t have. https://newrevenue.org/2017/07/02/nevadas-70-cent-per-gram-tax-on-marijuana-flower/

Now Nevada’s quick, if tormented, move to recreational sales (which started this month) is quicker than MA’s. Maybe a strong tax plan is part of a sound overall plan, so NV’s success with both is part of shrewd thinking. That’s pure speculation.

California Marijuana Tax 280E Conformity

2018 UPDATE: A.B. 420 failed to pass, and is dead for the moment.

California is considering letting individuals deduct all marijuana business expenses on California state income tax returns. The bill is A.B 420. A hearing is scheduled for July 12. http://sgf.senate.ca.gov/agenda

The real money here is in pass-through entities – S Corps, LLCs, and partnerships. These taxpayers get federal 280E treatment on California returns– they can deduct only cost of goods sold. California corporations can deduct all expenses. Here’s a long explanation of that California anomaly: https://newrevenue.org/2015/05/15/technicalities-of-california-marijuana-advertising-discrepancy/

The California Blue Ribbon Commission on marijuana legalization mentioned a possible rationale for part of California’s 280E nonconformity for individuals – as a way to limit advertising that opponents of legalization object to: Continue reading “California Marijuana Tax 280E Conformity”

Nevada’s 70-cent per gram tax on marijuana flower

Nevada taxes marijuana like Colorado, with a de facto weight tax (and a percentage-based retail tax). Alaska taxes only by weight. So three of the five states collecting marijuana taxes now are doing so by weighing every gram (Washington and Oregon tax only by percentage of retail price). UPDATE: California taxes by weight, too. The Tax Foundation’s strange claim that taxing by anything other than price is “untenable” loses even more credibility. After all, price taxes have almost no place in federal alcohol taxation. States stick to volume for alcohol, too, in general.

UPDATED RATES JUNE 2018:

Nevada taxes marijuana by weight, de facto, with these categories and current rates:

Flower — 75 cents a gram

Trim — 20 cents a gram

Small bud — 50 cents a gram

Wet whole plant — 7 cents a gram.

NV taxes by the unit

immature plants ($15)

seeds (($0.90)

pre-rolls ($0.75)

Those are calculated, as described below, from this data: https://tax.nv.gov/uploadedFiles/taxnvgov/Content/Forms/Retail-Marijuana-Fair-Market-Value-Jan-1-2018.pdf

Like Nevada, Colorado has seven categories, too. https://newrevenue.org/2015/10/12/beyond-bud-trim/

ORIGINAL DATA: Nevada starts with a percentage rate. Nevada’s new tax law, passed by the Legislature and effective July 1, 2017, taxes all cannabis, medical and adult-use, at “15 percent of the fair market value at wholesale of the marijuana.” https://www.leg.state.nv.us/App/NELIS/REL/79th2017/Bill/5688/Text.

That’s in addition to the 10-percent retail tax, which applies only to adult-use product, not to medical cannabis.

“The Fair Market Value at Wholesale is utilized by the Department in levying the wholesale excise tax imposed pursuant to NRS 453D.500 on the sale of marijuana by a marijuana cultivation facility.” https://tax.nv.gov/uploadedFiles/taxnvgov/Content/FAQs/Fair%20Market%20Value%20at%20Wholesale_July_1_2017.pdf

“The Department determined that the excise tax upon wholesale sales of retail marijuana can effectively be levied upon seven product categories:

1. Flower

2. Small Bud

3. Trim

4. Wet Whole Plants

5. Immature Plants

6. Pre-Rolls

7. Seeds.”

The prices to be multiplied by the 15-percent rate include $2,145 per pound for flower and $631 per pound for trim. So the tax per gram is 70 cents for flower and 21 cents for trim. (The per-pound tax, at 15 percent of $2,145, is $321.75, and there are some 453 grams in a pound.) The chart, with several more categories, is at https://tax.nv.gov/uploadedFiles/taxnvgov/Content/FAQs/Fair%20Market%20Value%20at%20Wholesale_July_1_2017.pdf. NOTE: Those per-pound rates have been updated: https://tax.nv.gov/uploadedFiles/taxnvgov/Content/Forms/Retail-Marijuana-Fair-Market-Value-Jan-1-2018.pdf Continue reading “Nevada’s 70-cent per gram tax on marijuana flower”

Oregon marijuana data from Beau Whitney

Oregon economist Beau Whitney’s early 2017 document, “Cannabis Employment Estimates” for the Oregon House Committee on Economic Development and Trade, is public, Continue reading “Oregon marijuana data from Beau Whitney”

Caulkins on marijuana taxes

My friend Jon Caulkins has a useful and thoughtful article on marijuana taxation here. Jon and I were among the co-authors of the RAND Report, “Considering Marijuana Legalization: Insights for Vermont and Other Jurisdictions.” I don’t agree with all of Jon’s new article, but I agree with a lot. (Some of it is line with my recent article in thehill.com.)

Here are some excerpts from Jon’s article:

“Marijuana prohibition is tottering, and procrastinating on doing the hard work of thinking through tax principles will more or less ensure a bad replacement.”

“The states leading the legalization charge have enacted primitive taxes that will fail as marijuana prices fall because they are computed as a percentage of value.” Continue reading “Caulkins on marijuana taxes”

Massachusetts Marijuana Tax Compromise

Here is an excerpt from my letter to the Editor of the Boston Globe, just published online:

In November, Massachusetts voters approved a 12 percent marijuana tax that would undercut the black market, but the House has proposed a 28 percent rate, in line with what other states collect.

Both sides are right — at different times. The marijuana market is a moving target, and needs a moving tax rate. As time goes on, pretax prices will fall, and the black market will weaken. So taxes can go up.

A solution is at hand — provided by proponents of marijuana legalization in federal bill S.776, the Marijuana Revenue and Regulation Act: Schedule rate increases to phase in year by year.

If increases come too fast, the Legislature can cut taxes. That avoids the problem of having legislators vote to raise taxes as needed, which is like cutting off a cat’s tail an inch at a time. Do it now and get it over with. Continue reading “Massachusetts Marijuana Tax Compromise”

Colorado marijuana taxes keep dropping

Colorado’s marijuana producer tax has hit an all-time historically low rate of 43 cents per gram on flowers (bud).

For vertically integrated companies, that 43-cent rate is arrived at by taking the statutory tax rate of 15 percent and multiplying it by per-gram Average Market Rates (AMRs) – market prices. So the nominal percentage-of-price tax is de facto based on weight. Since market prices keep dropping, taxes do, too. Which is primitive. Continue reading “Colorado marijuana taxes keep dropping”

Marijuana taxes and testing

As a tax person, I got involved in marijuana policy in 2009, since I figured that prohibition might not stand the test of time – and that whatever replaced prohibition would have revenue for the public. One of the problems with taxing marijuana is that heavy taxation can stifle the legal market, and thereby help the black market.

Well, it turns out that testing marijuana, at least at first, can create the same problem – high prices that consumers pay for legal product.

Here’s what happened in Oregon, according to an official and well-researched California report:

“Legal cannabis prices rise by 27%–39% in the two-month span after testing rules take effect. Revenue falls by $23,500 per dispensary due to supply constraints. Half of legal segment ($187.5 million) shifts back to illegal market. The illegal market grows from 50% to 75% while the legal market falls from 50% to 25%.” Continue reading “Marijuana taxes and testing”

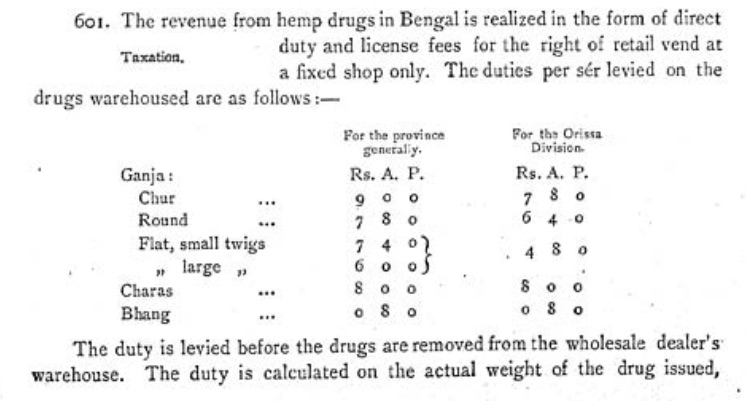

World’s 1st marijuana taxes

The world’s first cannabis taxes were collected in 19th century India, so far as I know, and Dale Gieringer of California NORML, who is way ahead of me on this history, indicates that that is the case. This chart, from the 1894 Report of the Indian Hemp Drugs Commission, is for Bengal, and shows rupees (currency unit, plus subunits) per ser (about a kilogram), collected at wholesale. The Bengal model was followed generally elsewhere in British colonial India.

As in Colorado today with bud and trim, different cannabis products were taxed at different rates. http://digital.nls.uk/indiapapers/browse/pageturner.cfm?id=74574724

From Wikipedia: An anna was a currency unit formerly used in India and Pakistan, equal to 1/16 [1] rupee. It was subdivided into 4 paisa or 12 pies (thus there were 64 paise in a rupee and 192 pies)…

Thanks to the National Library of Scotland for posting this public domain material.

Current conversion standard, from Wikipedia:

| Indian System | Metric System |

| 1 Tolä | 11.664 g |

| 1 Sèr (80 Tolä) | 933.10 g |

| 1 Maund (40 Sèr) | 37.324 kg |

Backfilling Cannabis Legalization History

The first footnote in my 2011 State Tax Notes article, Laws to Tax Marijuana, was this:

1 An extensive list of [marijuana legalization] proposals appears at Richard Evans, ‘‘Cannabis Taxation & Regulation,’’ available at http://cantaxreg.com/, under ‘‘Legalization Proposals’’ (last visited Dec. 7, 2010). This site is probably the most comprehensive compilation of information about laws to tax marijuana.

That link has expired along with cantaxreg.com, so the history would be hard to trace, but Dick Evans graciously provided its contents (updated somewhat) for me to post for all comers in the public domain: Continue reading “Backfilling Cannabis Legalization History”

Speaking to Southeastern Association of Law Schools meeting

Boca Raton, August 6, 2017

Discussion Group: Growing Cannabis Law: When Grass Becomes Cash

Cannabis a/k/a marijuana, grass, pot, weed law-reforms are sprouting throughout the country. Many states now permit restricted medicinal or recreational use, possession, sale, cultivation, and transportation, creating a cash-crop business opportunity. Yet federal law still prohibits cannabis activities Continue reading “Speaking to Southeastern Association of Law Schools meeting”

Testing Marijuana for Pesticides, continued

Here are new proposed testing regulations in California — but now I follow up on a recent post, where I said that while detecting cheating in folks who test marijuana for THC might be tricky, detecting cheating in folks who test marijuana for pesticides would be a snap. Just see if follow-up testing detected any pesticides; if so, start worrying.

But a chemist friend lets me know that there is more to it:

+++++

I differ in the pesticide opinion at the end of the article.

In science, there is no ‘zero’, there is only ‘less than’ or ‘not detected’. Continue reading “Testing Marijuana for Pesticides, continued”

Corva’s attack on cheating on marijuana plant testing

Testing companies gain customers if they can report falsely high THC in cannabis plants — and charge low prices. A friend says she quit the testing business because as an honest tester she was losing business to cheaters.

Thanks to Bob Young of the Seattle Times for brining Dr. Dominic Corva’s write-up to my attention. (This blog doesn’t have enough readers to scoop him.)

My friend Dr. Corva looks at the cannabis testing problem in Washington. His full write-up is here: http://cannabisandsocialpolicy.org/taming-thc-inflation-silver-bullet/.

I think Dr. Corva is a smart and conscientious advocate and thought leader, and I’m always interested in what he is thinking.

Dr. Corva’s Proposal:

“Normalize lab results by lab, and require only the percentile of each result to be listed on the package rather than a precise percentage.”

He elaborates on the problem this way: Continue reading “Corva’s attack on cheating on marijuana plant testing”

California clean-up bill does not fix tax blunder

California Board of Equalization elected Member Jerome Horton came up with an October surprise to illustrate a tax weakness in Prop 64, the California marijuana legalization initiative. That weakness didn’t prevent its passage, but it lingers. And a new 79-page clean-up bill does not fix it.

Member Horton alleged that a tiny, technical, last-minute drafting change in the California 2016 marijuana initiative could cost the state $50 million, starting in November. Indeed, the Board of Equalization has adopted his view and officially confirmed that the current sales tax on medical marijuana just disappears – for a while.

I don’t know how anyone would have standing to sue to reverse that ruling. So, apparently, unless the Legislature acts, the total tax on medical cannabis, over time, will be:

— 7.5%, (through the November 8 Election) then

— 0% (from certification of ballot results through 12-31-17), then

— 15% plus weight tax (starting 1-1-18).

For details, see this old post: https://newrevenue.org/2016/11/12/5032/.

Continue reading “California clean-up bill does not fix tax blunder”

Marijuana legalization grows closer with Senate tax proposal

Full article is at the link here. Intro to new piece for thehill.com is:

Want to legalize marijuana federally? Propose sensible taxes on the drug.

That’s the tactic of a new bill from two Oregon Democrats: House Ways

and Means Committee member Earl Blumenauer and ranking Senate Finance Committee member Ron Wyden. It takes on tough questions: What should a marijuana tax measure? Should it tax medical marijuana? The Marijuana Revenue and Regulation Act (MRRA) provides thoughtful answers.

What to tax?

The 64-page bill, S. 776, and House companions H.R. 1823 and 1841, starts out problematically, taxing marijuana by price for a five-year transition period, but ends up brilliantly, with sophisticated weight-based taxes for the long run. A companion bill repeals the useful current tax on advertising. Continue reading “Marijuana legalization grows closer with Senate tax proposal”

Back to DC

Moving back to in DC in May to become the first executive director of Stop Repatriation Tax Amnesty. “It’s No Holiday. Spread the Power. Share the Wealth.” Small business funding has come through. Continue reading “Back to DC”