I never met a sin tax I didn’t like, and I thought the self-styled socially conservative Republicans who control North Carolina might agree with me. But some of them are are soft on alcohol, because a prominent bill (to be fair, a bipartisan bill but with lots of Republican support) Continue reading “Alcohol tax cuts proposed in North Carolina”

Month: March 2013

An Unworkable Marijuana Tax in Colorado

As legalization of marijuana proceeds in fits and starts, the Colorado Task Force Report would impose at tax at the producer level while mandating vertical integration — combining the producer and retailer functions — so that every transaction requires determination of an arm’s-length inter-company price. That’s a recipe for chaos, involving the wishfully named arm’s-length method of guessing at tax pricing, a tool grown so feeble that it has turned the international tax schemes of the mightiest nations into laughingstocks.

Tax income or tax carbon?

My feeling about the income tax is that since we aren’t making it work after all this time (double Dutch sandwiches, tax havens, carried interest, the facially unconstitutional minister of the Gospel rule of Code section 107), I’d rather study something else.

Carbon is trivially easy to measure and remarkably easy to detect. But a carbon tax Continue reading “Tax income or tax carbon?”

Tax marijuana by potency? In one case, maybe

Trying to tax marijuana plant material on the basis of its potency (say, THC content) may be impractical because different labs routinely report wide variances in measured potency from a single sample.

But there’s a processed marijuana product that may be fungible enough for a potency tax: “concentrated cannabis oils, known in various states as ‘butter’, ‘shatter’, ‘wax’, and ‘BHO’.” That product looks fungible to me – video Continue reading “Tax marijuana by potency? In one case, maybe”

Tax marijuana by potency? Probably not

[UPDATE 4 September 2018: I’ve challenged people over and over, including at conferences and on twitter, to name a jurisdiction that taxes tobacco by nicotine content, and no one has.]

I was considering potency as a tax base in Laws To Tax Marijuana for a variety of reasons – mainly that it correlates with intoxication, which must be why society disfavors marijuana. (It’s more complicated than that . . .)

But marijuana is not fungible (except maybe some processed liquid products), and labs trying to measure THC, the primary intoxicant, show huge variances in results among themselves. You need a clear number to apply tax to, and those results aren’t clear enough.

Similar variances turn up for cigarettes, Continue reading “Tax marijuana by potency? Probably not”

Regulatory Capture of the OECD

My friend Joe Andrus (from my years in international tax policy) looks like the hero in this story: Multinational corporations stashing cash in tax havens (and avoiding tax in other ways, too) had bankrolled and influenced the Organization for Economic Cooperation and Development to the point that it was “in the pocket” of bad tax policy. Now Joe and others Continue reading “Regulatory Capture of the OECD”

The cover charge shift maneuver for retail-level excise taxes on consumables

A retail-level tax on a commodity presents lot of problems, like this one, suggested by the authors of Marijuana Legalization: What Everyone Needs to Know: A marijuana ‘”bar” could set low per-joint prices and derive most of its revenue from a cover or entertainment charge.

A response to that maneuver shows up in today’s WSJ: “In 1944, a new wartime ‘cabaret tax’ went into effect, imposing a ruinous 30% Continue reading “The cover charge shift maneuver for retail-level excise taxes on consumables”

Conference on marijuana revenue: List of issues

The Center for New Revenue is in the early stages of thinking about a conference on marijuana revenue that would assemble folks from the entire spectrum of views on legalization. Here is a draft list of issues:

Monopoly vs. Taxation

Whatever the advantages of the monopoly model, most states are choosing tax and regulate instead. But Oregon’s ill-conceived Continue reading “Conference on marijuana revenue: List of issues”

Carbon tax: Asking the easy questions

Three Democrats in Congress are asking for answers to easy questions about a carbon tax (like what should the rate be and what should we do with the money). But they aren’t facing up to this problem: If I pay tax because my manufacturing plant uses carbon to make stuff and my foreign competitor pays no tax, how does America level the playing field?

At least they don’t overlook indexing – they go beyond it (Bravo!) with the second of their three questions:

“How much should the price per ton increase on an annual basis? Continue reading “Carbon tax: Asking the easy questions”

Some Secrets of 280E

Some marijuana businesses face a tax trap in Tax Code section 280E. Continue reading “Some Secrets of 280E”

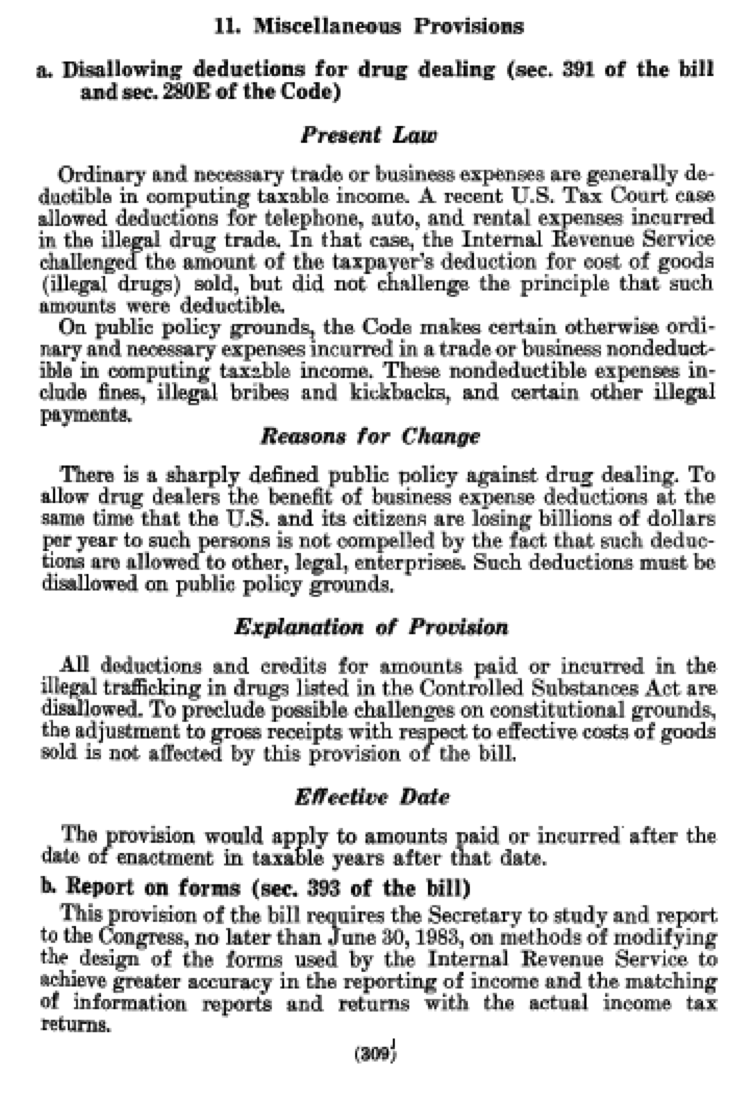

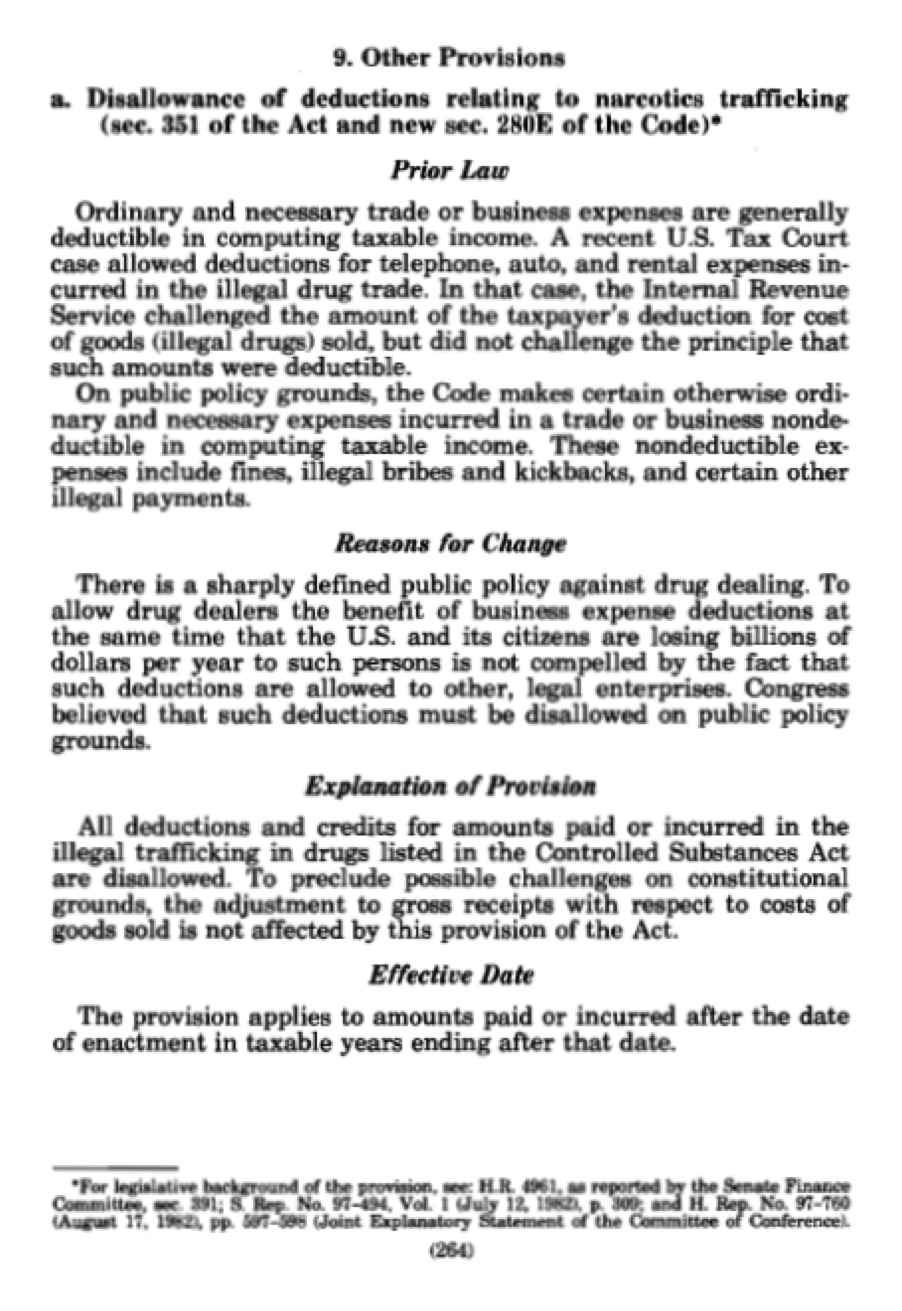

Marijuana Tax: Section 280E — Text, Senate Finance, and Joint Committee legislative history

First, here is the text of 26 U.S.C. § 280E, Expenditures in connection with the illegal sale of drugs:

No deduction or credit shall be allowed for any amount paid or incurred during the taxable year in carrying on any trade or business if such trade or business (or the activities which comprise such trade or business) consists of trafficking in controlled substances (within the meaning of schedule I and II of the Controlled Substances Act) which is prohibited by Federal law or the law of any State in which such trade or business is conducted.

(Text is from http://codes.lp.findlaw.com/uscode/26/A/1/B/IX/280E. Added by Pub. L. 97-248, title III, Sec. 351(a), Sept. 3, 1982, 96 Stat. 640. Public Law reference is from http://codes.lp.findlaw.com/uscode/26/A/1/B/IX/280E/notes.)

Second, here is legislative history, from the Senate Finance Committee Report, S. Rep. 97-494, downloadable from the huge file at http://www.finance.senate.gov/library/reports/committee/index.cfm?PageNum_rs=16 (volume 1), page 309 [oops! bad link as of 8 February 2018; try this: https://www.finance.senate.gov/imo/media/doc/srpt97-494.pdf].

That language is picked up with no meaningful change in the Joint Committee on Taxation’s 1982 Blue Book General Explanation of TEFRA: 1982 blue book.

That language is picked up with no meaningful change in the Joint Committee on Taxation’s 1982 Blue Book General Explanation of TEFRA: 1982 blue book.

UPDATE: 280E has its critics, but there are two sides to the story. Parents and others worry about advertising and marketing of cannabis, and 280E discourages marketing expenses, by making them nondeductible. More here (link to http://www.brookings.edu/blogs/fixgov/posts/2015/12/18-marijuana-adverstisement-tax-280e-oglesby.)

I interpret the so-called constitutional challenge as a red herring, intended to prevent overtaxation when vertical integration is not present – the cascading problem. https://newrevenue.org/2013/03/13/the-secrets-of-280e/#more-1735. Taxing gross receipts without a deduction for cost of goods sold wouldn’t be an income tax, which the Constitution explicitly authorizes, but it doesn’t need to be. A national sales tax would be constitutional.

NC poll shows 3 to 1 preference for state marijuana monopoly model over private sales

When faced with two models for legalization, state monopoly and taxed private sales, 58 percent of voters here in North Carolina (where the only retail seller of liquor is the state ABC monopoly) chose monopoly, 19 percent chose private sales, and 23 percent were undecided. The detailed results, from Public Policy Polling, are at NC Marijuana Polling March 2013.

The cross-tabs are interesting, too. In particular, monopoly prevailed overwhelmingly among all age groups other than the 18-29 group, where 36 percent chose monopoly, 36 percent chose private sales, and 28 percent were undecided. Monopoly doesn’t look like the wave of the future.

Revenue from a post-280E marijuana tax: Gross and net

I’ve written that federal and state revenue from taxing marijuana could be as much as $25 billion a year. http://www.huffingtonpost.com/pat-oglesby/a-way-marijuana-dilemma_b_2490720.html. But a revenue estimate for a new marijuana tax would presumably involve revenue loss from repeal of unpopular section 280E, which disallows deductions for all expenses other than cost of goods sold. Repeal of section 280E could be costly.

Marijuana Tax: An Unintended Consequence of 280E – Fragmenting the Industry?

Premise: A fragmented industry is harder to supervise and regulate.

Here’s what may be a counterproductive incentive of 280E. Say Mom and Pop operate a marijuana business: Continue reading “Marijuana Tax: An Unintended Consequence of 280E – Fragmenting the Industry?”

Marijuana tax thinking: Still in its infancy

A property tax on marijuana trademarks and patents seems almost impossible to administer. Figuring the value of those intangibles requires estimating the income they would generate, in a circumstance of total uncertainty. But Washington State House Bill 1976, just introduced, would impose a tax of $3.60 per $1,000 “of assessed value Continue reading “Marijuana tax thinking: Still in its infancy”

Tax legislative lingo: Rush to recede

In Congressional Conference Committees reconciling House and Senate tax bills, in the 1980s, at least, staffs worked through spreadsheets listing conflicting provisions and the evolving state of play as the two Houses gradually came into agreement.

The typical state of play early on went something like this for a particular provision: House position: Senate recedes. Senate position: House recedes. Neither side

Tax legislative lingo: Underbrush

Back when I worked for Congress, 1982-90, tax legislation — or negotiations in Congressional Conference Committee — often started with what staff called “underbrush” — pieces of a bill that everyone could agree on. “Everyone” meant six or seven groups: majority and minority staffs of Ways and Means in the House and Finance Continue reading “Tax legislative lingo: Underbrush”