Here is my statement for the Oregon State Legislature’s Joint Committee On Implementing Measure 91 tonight: Oglesby Testimony Oregon 16 Feb 2015

Climbing indexed gas tax

In light of the suggestion in the RAND Report for Vermont of increasing tax rates on legal marijuana, it’s heartening to see Congressman Earl Blumenauer’s gasoline tax bill — https://www.congress.gov/bill/114th-congress/house-bill/680/text — taxing by the gallon, with year-by-year rate increases. The Reports suggests taxing marijuana by weight or potency — which is like volume (gallons) for gasoline. Here are Mr. Blumenauer’s rates for gasoline other than aviation gasoline–

“(I) for tax imposed before 2016, 18.3 cents per gallon,

“(II) for tax imposed during 2016, 26.3 cents per gallon,

“(III) for tax imposed during 2017, 30.3 cents per gallon, and

“(IV) for tax imposed after 2017 and before 2028, 33.3 cents per gallon,”.

And there is indexing for inflation: Continue reading “Climbing indexed gas tax”

Washington State marijuana tax collections

Washington State collects a 25 percent tax from processors/producers and another 25 percent tax from retailers.

So far, the retail tax brings in some 64 percent of the total from all those taxes; the ratio of the retail tax to the other taxes is 1.57 to 1. Continue reading “Washington State marijuana tax collections”

Mistakes in 2011 “Laws to Tax Marijuana”

Here are three big issues that I overlooked in “Laws to Tax Marijuana,” printed in State Tax Notes on January 24, 2011. The three biggest I’ve discovered so far, anyway. And a few small mistakes.

1. The high probability that collapsing prices will gut a percentage-of-price tax base. The 2015 RAND Report on Vermont puts it this way Continue reading “Mistakes in 2011 “Laws to Tax Marijuana””

280E and fees — Withdrawn and superseded

April 15, 2015: I take this back. A more useful post is here: https://newrevenue.org/2015/04/15/280e-and-fees-arkley/

++++++++++

Drafters of state marijuana revenue proposals might try to help the industry by making sure state taxes are federally income-tax-deductible under Code section 280E. That could be tricky. Lots more here.

State fees, as opposed to taxes, have a big advantage for states: A state can collect fees for licenses and applications and so on up front — to finance the operation of putting a new system in place. The state needs to spend money to make money, Continue reading “280E and fees — Withdrawn and superseded”

Alcohol Excises — Lowry

This Congressional Research Service document about alcohol excises is in the public domain but it’s so hard to find that I’m saving it here: Alcohol Excises — Lowry. A more general document is by the same author, Sean Lowry, is here or at https://newrevenue.org/wp-content/uploads/2014/11/federal-excise-taxes-lowry.pdf, His piece on marijuana excises, with Jane Gravelle, is here or at https://newrevenue.org/wp-content/uploads/2015/01/fed-mj-tax-r43785.pdf.

Dynamic scoring for sin taxes

What will happen if tax laws change? Republicans, newly in control of Congress, want to change the rules. Here are the stakes: the official predictions of what will happen determine whether a tax bill is a budget-buster – so maybe if it can pass or not.

CBO and Joint Tax have been not using, for budget purposes, so-called dynamic scoring, but the new 114th Congress is working on that. “Current rules require calculating a policy’s direct cost to the government, which includes looking at how affected individuals and firms would react to the policy. But dynamic scoring goes further by requiring that budget estimates also take into account how policies could affect the total size of the economy.” http://www.whitehouse.gov/blog/2015/01/06/dynamic-scoring-not-answer. Continue reading “Dynamic scoring for sin taxes”

6 Ps for marijuana tax bases

Beau Kilmer, beneficent captain of the RAND team that wrote the Report Considering Marijuana Legalization: Insights for Vermont and Other Jurisdictions, has come up with 9 Ps to help analyze marijuana legalization: Production, profit, promotion, prevention, penalties, potency, purity, price, and permanency. (I’d add “Patients,” to address whether tax exemption for medical marijuana makes sense, but that’s a side issue, addressed here. And “Patience” will come in handy.)

As a corollary to those Ps, here is a way to think about marijuana’s tax base (the measuring stick to which a numerical rate is applied), discussed at pages 76-87 of that Report, using six more Ps:

Considering Marijuana Legalization — RAND

Insights for Vermont and Other Jurisdictions: by Jonathan P. Caulkins, Beau Kilmer, Mark A. R. Kleiman, Robert J. MacCoun, Gregory Midgette, Pat Oglesby, Rosalie Liccardo Pacula, Peter H. Reuter.

Here and http://www.rand.org/pubs/research_reports/RR864.html. My revenue supplement is at Vermont Supplement.

Extreme marijuana monopoly

At one extreme is a seed-to-sale monopoly. To provide security, the state could put the growing outdoors, surrounded by fences and cameras, in the middle of the campus of a land grant University, or at the state’s version of a College of Agriculture and Life Sciences. To identify legal product, scientists might develop genetic or biological markers.

Tom Barthold

Congratulations to Tom Barthold, who stays on as Chief of Staff of the Joint Committee on Taxation, who keeps his job. http://www.bloomberg.com/news/2015-01-12/republicans-retain-tax-bill-scorekeeper-picked-under-democrats.html. We were on staff at the same time, and I have only good things to say about him.

Tax jet fuel

Here’s an excise tax that’s not regressive. Federal jet fuel rates now range from “$0.219 for general aviation such as private jets to $0.044, for commercial aviation.” http://taxfoundation.org/blog/combined-effective-commercial-jet-fuel-tax-rates-and-fees-state

States race to the bottom to attract flights, naturally enough, so they can hardly lead the way here. A federal tax increase would either cut emissions or raise revenue. Poor folks don’t fly much, even commercially. The hurt from this tax won’t be as concentrated on the wealthy as taxing carried interest appropriately, but it’s hardly regressive.

Gravelle-Lowry Report: “Federal Proposals to Tax Marijuana: An Economic Analysis”

Here is the text: Fed mj tax R43785

Taxes Help Legalization

A Colorado poll asked, “What has been the greatest benefit of legalization?” — and got these answers:

If you can’t see the image: Continue reading “Taxes Help Legalization”

If you can’t see the image: Continue reading “Taxes Help Legalization”

Supplemental Thoughts about Revenue from Marijuana in Vermont

Supplemental Thoughts about Revenue from Marijuana in Vermont, 16 January, 2015 in pdf, by Pat Oglesby, supplements “Considering Marijuana Legalization: Insights for Vermont and Other Jurisdictions,” a RAND Corporation Report issued January 16, 2015. That Report is here: http://www.rand.org/pubs/research_reports/RR864.html and here: Considering Marijuana Legalization, RAND, 16 January 2015

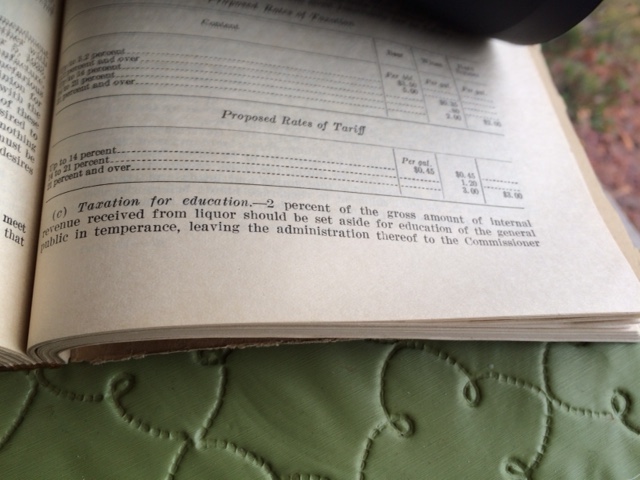

Dedicate taxes to temperance — 1933

The Federal Bar Association of New York, New Jersey, and Connecticut urged that 2 percent of new federal liquor taxes go for temperance education – from page 301 of Tax on Intoxicating Liquor, Hearings Before the Committee on Ways and Means, House of Representatives and the Committee on Finance, United States Senate, 73d Congress, Interim, 1st and 2d Sessions (Dec. 11-14, 1933). (Carryover page says “of Education.”)

The economic conditions of the Depression did not allow that diversion of revenue. But some of Washington State’s tax on marijuana does go for temperance education.

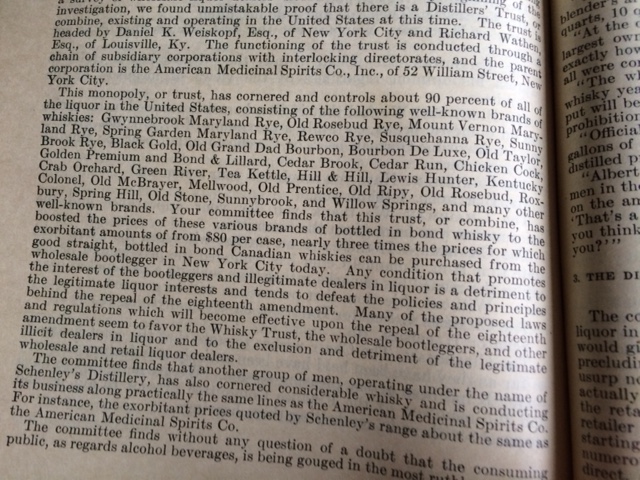

Black market price ratio 1933

Lewis Landes, lawyer for the Wholesale Liquor Dealers Committee of New York City, accused a “Distillers’ Trust” of keeping legal prices to wholesalers “exorbitant” — about three times the black market price. This is from page 296 of Tax on Intoxicating Liquor, Hearings Before the Committee on Ways and Means, House of Representatives and the Committee on Finance, United States Senate, 73d Congress, Interim, 1st and 2d Sessions (Dec. 11-14, 1933).