My friend Dr. Dale Gieringer, head of California NORML, writes (and authorizes me to post):

Hi Pat –

The illicit market is going great guns here in CA. Continue reading “Over-regulating cannabis in California?”

My friend Dr. Dale Gieringer, head of California NORML, writes (and authorizes me to post):

Hi Pat –

The illicit market is going great guns here in CA. Continue reading “Over-regulating cannabis in California?”

I’m to give a guest lecture in my old friend from international tax days Peter Barnes’s VAT and Sales Tax Class at Duke Law School today on Excise taxes, especially alcohol and cannabis. Here are the 100 slides I’m still tinkering with (download):

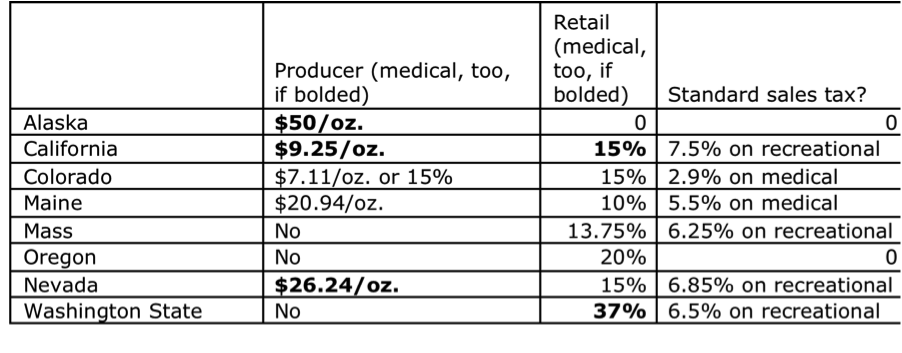

Master Sales and VAT Duke 2018 beyond the $

Note the bolding, above. Nevada taxes all cannabis de facto by weight; Colorado taxes producers by weight unless there is an arm’s-length sale.

Oregon’s 20-percent number reflects a 17-percent state tax and universally adopted 3-percent local taxes. Otherwise local taxes are more of a patchwork, and are ignored. Colorado and Nevada have nominal 15-percent producer taxes. Colorado converts its tax to a weight base for related party or vertically integrated cases. https://newrevenue.org/2017/07/23/is-colorados-new-marijuana-tax-leaky/. Nevada converts to a weight base for all cases. https://newrevenue.org/2017/07/02/nevadas-70-cent-per-gram-tax-on-marijuana-flower/

Details on Washington: Exemption from 6.5% standard sales tax for medical marijuana: https://dor.wa.gov/find-taxes-rates/taxes-due-marijuana. Obligation to pay 37 percent excise tax on medicalamarijuana: https://dor.wa.gov/sites/default/files/legacy/Docs/Pubs/SpecialNotices/2016/sn_16_med_endorsement.pdf.

Senators McCaskill and Shaheen have a bill to stop tax deduction for prescription drug ads. The American Medial Association and my drug policy friends approve. This stoppage would treat Rx drug ads like marijuana ads — and nudge against them via taking away this tax break. Maybe freedom of speech (for marijuana, in state Constitutions) won’t let us stop the ads, but we don’t have to subsidize them.

Proposed section 280I text includes:

No deduction shall be allowed under this chapter for expenses relating to direct-to-consumer advertising of prescription drugs for any taxable year.

Why not do the same for alcohol, tobacco, and opioids?